The water damage guarantee of a multi-risk home insurance policy is not limited to a line in a table of guarantees. Its application conditions, exclusions, and compensation mechanisms contain contractual subtleties that escape most policyholders, revealing themselves at the time of the claim.

Maintenance Obligations and Forfeiture Clauses in Recent Contracts

Since 2023-2024, several insurers (Groupama, Allianz, MAAF among others) have tightened the conditions for covering water damage to include explicit maintenance obligations. Periodic replacement of supply hoses, inspection of sealing joints, installation of leak detection devices: these requirements are now included in the general conditions or information notices.

Recommended read : Everything You Need to Know About Zalando Referral: Tips, How It Works, and Benefits to Seize

Failure to comply with these obligations constitutes a reason for reducing compensation or even outright refusal. We observe that these clauses are rarely read at the time of subscription. The policyholder discovers their existence during the assessment when the technician finds a ten-year-old punctured hose or a bathtub seal that has deteriorated over several years.

In practice, to fully understand the specificities of the water damage guarantee, we recommend rereading the “policyholder obligations” section of your general conditions. Check for the presence of any clause linking the guarantee to documented regular maintenance.

Related reading : Salary, bonuses, and benefits: everything you need to know about the compensation of researchers at CNRS

Boundary Between Water Damage Guarantee and Natural Disaster Guarantee

The incidence of home insurance claims related to extreme weather events has significantly increased since 2022. Intense rains, violent storms, runoff: these phenomena cause infiltrations and blockages in the private drainage network that blur the boundary between two distinct guarantee regimes.

A sewer backup caused by a storm does not automatically fall under the water damage guarantee. If the event is subject to a ministerial order declaring a natural disaster, the CatNat regime applies, with its specific legal deductible. Without an order, the claim falls back under the classic water damage category, but the insurer may invoke the exclusion related to “runoff water” if it is included in the policy.

This gray area generates increasing disputes. France Assureurs highlights the significant rise in climate-related claims, a substantial portion of which involves flooding and infiltrations combined with the private network. The policyholder should check whether their contract explicitly covers infiltrations due to runoff or limits them to storm or CatNat coverage only.

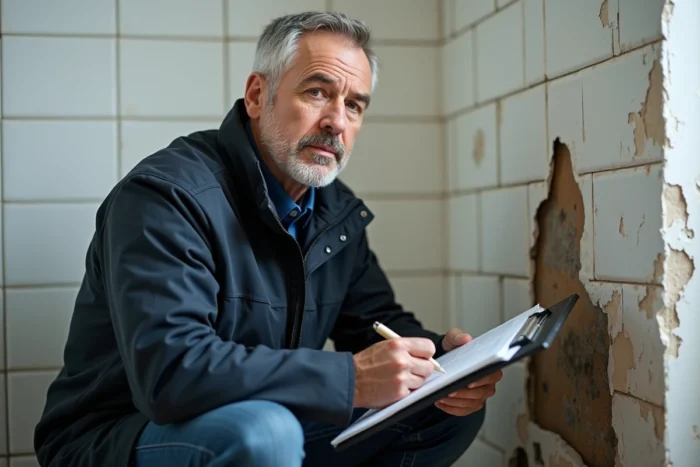

Infiltrations Through Roofs and Walls: The Trap of Maintenance Neglect

Water infiltrations through roofs, walls, or windows are only covered if they result from a sudden and accidental event. An infiltration due to wear and tear or lack of maintenance is systematically excluded. The burden of proof for the accidental nature lies with the policyholder.

In a co-ownership situation, the situation becomes more complicated: infiltration through the roof falls under the building’s insurance (common areas), but damages within the apartment fall under the individual contract of the occupant. Coordination between the two contracts is governed by the IRSI convention, which organizes the management of claims below a certain threshold.

Leak Detection Guarantee: A Distinct Coverage to Verify

Recent contracts include or strengthen a specific leak detection guarantee, distinct from the repair of the water damage itself. This guarantee covers intervention costs (plumber, non-destructive detection by thermal camera or tracer gas) as well as the restoration of elements damaged by the investigations (opening of walls, removal of tiles).

The absence of this guarantee in a contract exposes the policyholder to costs that can sometimes exceed those of the initial claim. We recommend checking three points in your contract:

- Is leak detection covered as a standalone guarantee or only as an option?

- Does the indemnity limit cover non-destructive detection, which is significantly more expensive than the classic method of opening?

- Is the restoration of elements removed for detection (tiles, drywall, false ceiling) included or limited to a flat rate?

IRSI Convention and Distribution of Coverage Between Insurers

The IRSI convention (Compensation and Recourse for Building Claims) governs the management of water damage involving multiple parties in the same building. It defines which insurer manages the case and advances compensation, based on the amount of the claim and the location of the damages.

The insurer of the occupant of the damaged premises manages the case below the threshold set by the convention. This mechanism speeds up processing but requires the policyholder to report the claim to their own insurer, even if the leak originates from a neighboring unit. Failing to adhere to this reporting logic delays compensation.

Friendly Report and Reporting Deadline

The deadline for reporting a water damage claim is set at five working days. The friendly report of water damage, to be filled out between the parties involved (the source of the leak, the victim, possibly the property manager), constitutes the central document of the case. An incomplete or poorly filled report complicates coverage and may delay the assessment.

Points not to overlook on the report:

- Precisely identify the presumed origin of the claim (room, equipment, affected pipe)

- Have the report signed by all parties involved, including the property manager if common areas are involved

- Attach dated photos of visible damages and keep damaged items until the expert’s visit

Compensation: Use Value, Replacement Value, and Deductible

The method of compensation varies according to the contracts. Under use value, a depreciation coefficient is applied, sometimes significantly reducing the reimbursement for old furniture or coverings. Contracts with replacement value, which offer more protection, eliminate or cap this coefficient, but are more expensive in premiums.

The deductible, often flat-rate, is systematically applied. It remains the responsibility of the policyholder, regardless of the amount of the claim. For small water damage (ceiling stain, locally warped flooring), the deductible can absorb nearly all of the compensation.

Each home insurance policy defines its own limits for water damage coverage. Checking these before a claim, rather than after, is the only way to avoid an unpleasant surprise at the time of compensation.